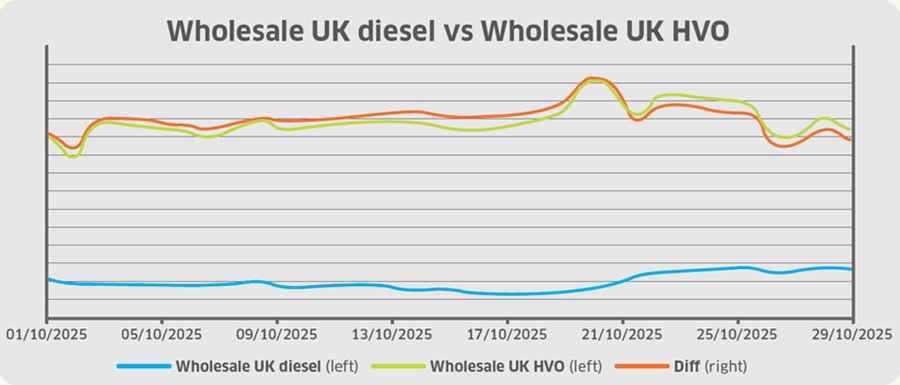

In October, wholesale UK diesel prices increased marginally from 52ppl to 55.5ppl (excluding duty) despite dipping to near 48ppl mid-month, largely tracking the underlying Brent crude benchmark.

Throughout October, persistent oversupply concerns weighed on oil prices, driven by OPEC+ output hikes. However, the group announced a modest output increase of 137,000 barrels per day at the beginning of the month, less than expected and alleviating concerns.

Increased optimism around a ceasefire in Gaza reduced the geopolitical risk premium, which also caused oil prices to fall. On 10 October, the Israeli military announced that a ceasefire began in Gaza as the “first phase” of a peace deal agreed by Israel and Hamas came into effect.

On the other hand, tensions between Russia and Ukraine escalated with large-scale drone attacks targeting Kyiv. Ukraine soon retaliated with strikes on Russian refineries, causing supply concerns. Although Trump and Putin were set to meet to discuss the war, the US cancelled a Budapest summit following Russia’s firm stance on hardline demands regarding Ukraine.

Furthermore, softer demand projections for 2025 and 2026 continued to dampen prices. However, they surged by 5% on 23 October after the US imposed sanctions on Russia’s major oil producers Rosneft and Lukoil to pressure Moscow into ending the war in Ukraine.

Towards the end of the month, US Treasury Secretary Scott Bessent announced he had reached a “substantial framework” with Chinese Vice Premier He Lifeng to avoid 100% US tariffs on Chinese goods.

However, investors remained sceptical that the decision marked an end to the trade war. Finally, the market anticipated another modest oil output increase by OPEC+ in its 2 November meeting.

GBP depreciated from US$1.350 to US$1.314 during October, trading around its weakest level since April as market sentiment was weighed down by fiscal uncertainty and expectations of looser monetary policy in the UK.

At the beginning of the month, a strengthened US dollar pressuring the pound sat alongside investor caution ahead of the UK’s November budget, with concerns that tax hikes and fiscal tightening could further strain the fragile economy.

By mid-October, GBP briefly rebounded after forecasts by the International Monetary Fund suggested the UK would be one of the fastest-growing advanced economies, and GDP data showed modest 0.1% growth in August. However, the recovery was short-lived as weak wage data and inflation concerns resurfaced.

In addition, the pound faced renewed weakness after government borrowing exceeded forecasts by £7.2 billion, while inflation remained stuck at 3.8%, reinforcing expectations that the Bank of England might cut interest rates.

In the final week of October, GBP fell sharply from US$1.332 to US$1.312 after Chancellor Rachel Reeves confirmed that both tax increases and spending cuts were under consideration for the upcoming budget.

Although the US Federal Reserve cut rates by 25 basis points, the dollar remained firm as Chair Jerome Powell signalled caution over further easing, amplifying GBP’s decline amid growing UK fiscal and economic concerns.

Wholesale UK renewable diesel (HVO) increased in price marginally from almost 151ppl (excluding duty and Renewable Transport Fuel Certificate (RTFC) benefit) to 152ppl by the end of the month, largely due to persistently strong demand guided by the EU Renewable Energy Directive (RED).

Investors are also keeping an eye on developments in the Netherlands after it started exploring the possibility of extending its renewable transport fuel targets under RED out to 2040 to better align with countries including France and Germany.

Meanwhile, a scheduled discussion of Germany’s proposals for transporting new EU biofuel targets into national law has been pushed back, adding to market concerns that a January 2026 deadline will be missed. The RED III draft law changes would lead to significant changes to Germany’s biofuel mandate; however, the delay could result in a slow start to Q4 without confirmation of the targets.

In other news, the International Energy Agency has revised upwards its 2030 biofuels demand growth forecast by 50% in its latest annual Renewables 2025 report, with supporting global policies contributing to increased demand.

On the supply side, over 2 million metric tonnes of additional sustainable aviation fuel and renewable diesel capacity will enter the market in 2026, supported by co-processing volumes, plant upgrades and refinery conversions, marking an increase of around 30% according to consultancy Energy Aspects.

Finally, the cost of blending biodiesel to UK B7 specification declined marginally from 7.9ppl to 7.6ppl, slightly decreasing the cost of meeting the Renewable Transport Fuel Obligation (RTFO). Meanwhile, the price of RTFCs rose from 26p per certificate (ppc) to beyond 27ppc, increasing the benefit that HVO consumers receive (assuming 100% of the RTFC benefit is passed on to the end-user).