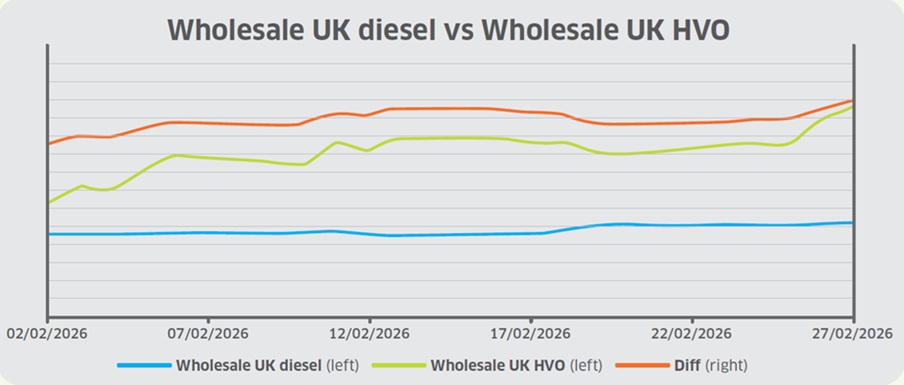

In February, wholesale UK diesel rose from 42.71ppl to 47.94ppl (excluding duty), largely tracking the underlying Brent crude benchmark that saw moderate gains throughout the month amid heightened geopolitical tensions and potential supply disruptions.

At the beginning of February, oil prices fell following optimism around potential negotiations between the United States and Iran on Tehran’s nuclear program, alongside reduced fears of immediate supply disruptions.

Diplomatic signals from President Trump and Iranian officials briefly eased risk premiums, with reports that Tehran was “seriously talking” with Washington.

However, Iranian vessels then challenged a US-flagged tanker transiting the Strait of Hormuz, a vital chokepoint for approximately 20% of the world’s oil exports, and the US downed an Iranian drone that “aggressively” approached a US aircraft carrier in the Arabian Sea.

Uncertainty persisted as the US sought broader talks on Iran’s missiles and regional activities, while Iran wanted to focus only on nuclear issues and sanctions relief.

In the Russia-Ukraine war, Kyiv reportedly agreed to a multi-tiered ceasefire enforcement plan for Russia with Europe and the US, aimed at strengthening compliance and monitoring, including rapid response measures, allied coordination, and escalation mechanisms for violations. However, two days of US-led peace talks ended without a breakthrough.

In the second week of February, the US issued fresh guidance to commercial vessels transiting the Strait of Hormuz, advising US-flagged ships to stay as far as safely possible from Iranian territorial waters.

Investors weighed US-Iran tensions against persistent oil oversupply concerns, alongside a weakened demand outlook, indicated by building US crude inventories reported by the Energy Information Administration.

A second round of US-Iran nuclear talks occurred in mid-February after Tehran signalled willingness to make concessions on its nuclear program if Washington engages on sanctions.

Oil prices cooled following talks in Geneva, after Iran said it had reached an understanding of the main principles of a deal. Russia-Ukraine talks also continued, but negotiations ended abruptly after just two hours, causing oil prices to surge.

In the final week of February, oil prices slipped as markets reacted to global economic uncertainty after President Trump raised a temporary blanket tariff on US imports from all countries from 10% to 15%, despite the Supreme Court ruling that his previous sweeping tariffs were illegal.

Meanwhile, US-Iran developments saw Tehran’s foreign minister state that a diplomatic “win-win” solution with Washington was within reach, and President Trump suggested he would prefer reaching an agreement with Iran rather than conducting military strikes.

However, on 28 February, the US and Israel conducted coordinated strikes targeting Iran’s leadership, security forces and nuclear programme and missile sites, causing both military and civilian casualties.

The death of Iranian Supreme Leader, Ayatollah Ali Khamenei, was confirmed, prompting retaliatory missile and drone strikes on Israel, US bases and Gulf states, with reported civilian and US military casualties.

The unprecedented strikes have intensified concerns of supply disruptions in the Middle East, with market attention focused on the Strait of Hormuz.

Multiple vessels have been targeted in the Arabian Gulf, and hundreds of tankers have dropped anchor, meaning that the strait is effectively closed, prompting major shipping companies to reroute via the Cape of Good Hope.

The conflict quickly expanded to a wider regional crisis after Iran-backed Hezbollah launched rockets and drones at the Israeli city of Haifa to avenge the killing of Iran’s Supreme Leader. To prevent further attacks on Israel, the Israel Defence Forces (IDF) ordered ground troops to “advance and seize additional strategic areas in Lebanon”.

Finally, Iranian strikes have targeted a major liquefied natural gas plant in Qatar, prompting state-owned QatarEnergy to suspend production, as well as Saudi Arabia’s giant Ras Tanura refinery, which halted operations as a precaution, further escalating regional energy tensions.

Despite UK diesel having closed 27 February at 47.94ppl plus duty, geopolitical tensions pushed oil prices significantly higher into March. As of 3 March they traded at the highest level since July 2024, and UK wholesale diesel prices increased by 35% compared to February’s close.

Looking ahead, President Trump said the US would do “whatever it takes” when asked how long the war with Iran could persist. With elevated tensions in the Middle East, concerns about prolonged disruptions to global trade are likely to continue driving significant near-term market volatility in March, pushing oil prices higher.

GBP depreciated from US$1.363 to US$1.345 throughout February. Early in the month, investors held a cautious stance ahead of key monetary policy decisions. Support for the dollar followed comments from Federal Reserve Chair Jerome Powell noting a clear improvement in the US economic outlook and signs of a stabilising labour market.

In the UK, inflation rose to 3.4% in December 2025 from 3.2% in the previous month, while the Bank of England held interest rates at 3.75%. Although the decision was widely expected, the narrow 5-4 vote and more dovish tone weighed on the pound.

Expectations of monetary easing grew after data from the Office for National Statistics showed modest Q4 2025 growth of 0.1%, rising unemployment at 5.2%, and easing wage pressures. Inflation subsequently fell to 3% in January, reinforcing market pricing for a 25-basis point rate cut by April, with economists projecting that rates could decline to 3% by year-end.

Meanwhile, political developments added further pressure to the currency. Prime Minister Keir Starmer faced renewed scrutiny following the resignation of his Chief of Staff, contributing to uncertainty despite public backing from senior ministers.

Although the pound briefly recovered towards US$1.350 amid periods of dollar weakness, it fell to US$1.345 by the end of the month.

Wholesale UK renewable diesel (HVO) prices (in reference to the HVO UCO Barges FOB ARA benchmark) increased significantly in February, from 131.49ppl (excl. duty and Renewable Transport Fuel Certificate (RTFC) benefit) to 158.10ppl, causing the differential to wholesale UK diesel to widen. Note: this is a wholesale settlement price comparison only, and does not reflect broader end-user pricing dynamics.

HVO price movements were driven by tightening supply and projections of stronger demand. In early February, prices firmed sharply after TotalEnergies shut a HVO unit, tightening supply and lifting ARA renewable diesel premiums. This outage reduced immediate HVO availability and pushed up short‑term pricing in northwest Europe.

On the demand side, toughening EU renewable fuel mandates are expected to deliver a boost as member states raise targets and reduce biofuel double‑counting. Notably, the German lower house of parliament scheduled a debate on new biofuel legislation for 26 February, marking a key step in updating biofuel laws.

Ahead of that, bioenergy associations urged the government to raise the 2027 fuel greenhouse gas reduction target and the cap on crop-based biofuels, which could sharply tighten the EU renewable fuel balance this year.

Meanwhile, US regulators said the final 2026-27 biofuel blending mandate is being sent to the White House and is expected to be finalised by the end of March, providing clarity on required biofuel volumes under the Renewable Fuel Standard.

Overall, multinational energy company Eni has forecast that global biofuel demand will climb by 25% this year, driven mainly by new renewable fuel targets in Europe and the US.

Finally, the cost of blending biodiesel to UK B7 specification fell marginally to 7.40ppl, slightly decreasing the cost of meeting the Renewable Transport Fuel Obligation (RTFO). Meanwhile, the price of RTFCs fell from 26.40 pence per certificate (ppc) to 24.40ppc, reducing the benefit that HVO consumers receive (assuming that 100% of the RTFC benefit is passed on to the end-user).