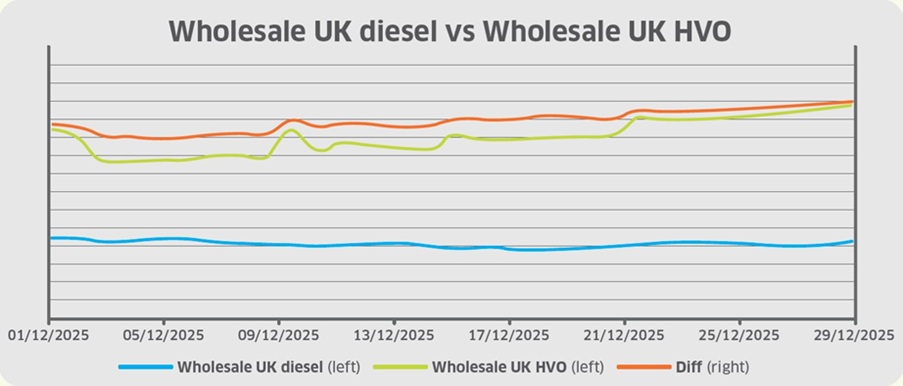

In December 2025, wholesale UK diesel prices declined from 44.87ppl (excluding duty) to 39.66ppl. That largely tracked the underlying Brent crude benchmark, which showed a downward trend throughout the month due to persistent oversupply concerns.

At the beginning of December, OPEC+ opted to maintain existing production levels for Q1 2026, partially alleviating oversupply concerns.

Additionally, heightened geopolitical risks provided some support to oil after President Trump threatened land operations to stop suspected drug traffickers in Venezuela. The country has since accused the United States of international piracy after it continued to seize sanctioned oil tankers.

In the Russia-Ukraine war, ongoing peace talks have so far failed to produce a definitive outcome. The conflict intensified after Putin threatened Europe over what he labelled “unacceptable” ceasefire demands, leaving investors sceptical that the war will end any time soon or that sanctions on Russian crude will be lifted as a result.

However, sentiment improved after President Zelensky met with EU leaders, while a separate peace proposal from the US, which reportedly involved restoring Russian energy flows to Europe, helped to ease supply concerns.

By mid-December, oil prices had dropped to their lowest level since March 2021 after Trump claimed that a peace deal was “closer than ever” – yet nothing has since been agreed.

Furthermore, weak demand sentiment was evident after economic data indicated ongoing strain in the world’s second largest crude consumer, China. Tied to persistent oversupply concerns, that caused oil prices to fall. Overall, oil recorded the largest annual decline in five years. Wholesale UK diesel prices fell below 40ppl (excluding duty) as a result.

GBP strengthened from US$1.325 to a two-month high of US$1.345 in December, supported by a weaker dollar, also contributing to lower wholesale UK diesel prices.

UK economic data showed that the manufacturing sector returning to growth, with the Purchasing Managers’ Index rising to 51.3, above 50 for the first time since September 2024.

Meanwhile, the Organisation for Economic Co-operation and Development suggested that UK inflation would remain among the highest in the G7, though it should start easing, while tax rises and spending limits following the autumn 2025 Budget could weigh on growth.

However, the Institute for Public Policy Research noted that historically high borrowing costs may be easing, supporting the pound.

Other data showed that domestic GDP contracted by 0.1%, marking four months without growth, while annual inflation slowed to 3.2% in November 2025, below the 3.5% forecast but still above the Bank of England (BoE) 2% target.

Unemployment rose to its highest since 2021 and wage growth slowed, reinforcing expectations of an interest rate cut. The BoE reduced rates from 4% to 3.75%, the lowest since January 2023.

In the US, jobless claims fell to their lowest since September 2022, with non-farm payrolls rising 64,000 in November after October’s 105,000 drop. The Federal Reserve also cut rates by 25 basis points to 3.50–3.75%, with officials divided over future policy. Overall, the pound has gained nearly 8% in 2025 despite economic challenges.

Wholesale UK renewable diesel (HVO) prices increased across December 2025 from 152.49ppl (excluding duty and Renewable Transport Fuel Certificate (RTFC) benefit) to 159.44ppl, despite falling below 144ppl on 4 December.

The European HVO market has seen increased consumption alongside relatively stable production, which has tightened supplies. Planned maintenance closures at both European and Chinese facilities during Q4 may continue to support prices early next year.

European HVO prices are unlikely to ease in 2026, with industry bodies forecasting continued strength as the market braces for higher blending targets next year. Likewise, higher premiums have been driven by stronger demand from obligated parties rushing to meet Renewable Energy Directive (RED) targets before the end of the year.

Furthermore, Germany and the Netherlands plan to remove double counting in 2026 as they implement RED III. That could significantly boost demand as higher absolute volumes of biofuels will be required to meet greenhouse gas reduction quotas, which then supports demand for drop-in fuels like HVO.

Finally, the cost of blending biodiesel to the UK B7 specification rose to 8.2ppl, slightly increasing the cost of meeting the Renewable Transport Fuel Obligation. Meanwhile, the price of RTFCs hovered around 26.5 pence per certificate, meaning the benefit that HVO consumers receive stayed the same (assuming that 100% is passed to the end-user).