Oil markets experienced significant volatility in April, with sharp price fluctuations driven primarily by developments in the Middle East. On 31 March, prices rose amid escalating fears of prolonged supply disruption, combined with United States President Trump suggesting that countries should “go to the Strait of Hormuz and just take” oil, exacerbating concerns of escalation.

However, oil prices declined by almost 15% in less than 24 hours after Trump suggested that US forces could withdraw from Iran in two or three weeks, while Iranian President Pezeshkian indicated Tehran’s willingness to end the war if guarantees were provided. Wholesale UK diesel closed at 86.88ppl (excluding duty) on 1 April.

On the second day of the month, wholesale UK prices surged by over 13ppl to trade above 100ppl, amid soaring oil prices on the back of fading hopes for a quick resolution to the Iran conflict, while Trump claimed the US would keep up attacks on Tehran without committing to a specific timeline to end the war.

After the Easter break on 7 April, the US president warned that “a whole civilisation will die tonight” unless Iran agreed a deal to end the war and reopen the Strait of Hormuz, marking a significant escalation in his threats.

The following day, Trump announced a delay to potential strikes, outlining a conditional two-week ceasefire with Iran linked to reopening the vital strait. Oil prices declined by 13% after the announcement, and wholesale UK diesel prices plunged by more than 17ppl.

On 17 April, wholesale UK diesel fell below 68ppl following reports that US and Iranian negotiation teams were set to return to Islamabad, with Trump claiming the US was “very close” to reaching a deal.

Iran’s foreign minister Abbas Araghchi also announced that the strait would be open for commercial vessels during the ceasefire period with the US. Meanwhile, a 10-day Israel-Lebanon ceasefire signalled a temporary pause in wider regional hostilities.

Trump extended the ceasefire on 21 April to allow further negotiations. However, tensions involving the strait remained unstable. Reports suggested repeated changes in shipping access, with restrictions reimposed soon after earlier reopenings, highlighting uncertainty surrounding the truce.

Towards the end of April, Trump announced a three-week extension of the Israel-Lebanon ceasefire following mediation. Meanwhile, the US and Iran remained deadlocked in efforts to end the war, and Washington rejected Iran’s latest proposal for a phased ceasefire.

A report that the US military was set to brief Trump on new military options in Iran caused oil prices to temporarily surge to a wartime high, before settling back down. Overall, wholesale UK diesel prices closed the month at 83.09ppl, fluctuating between above 100ppl and below 68ppl.

Despite tensions continuing to boost safe-haven demand for the US dollar, pressurising the pound, GBP appreciated from US$1.333 to US$1.359 throughout April as investors monitored monetary policy and domestic economic data releases.

At the start of the month, investors forecasted two interest rate hikes by the Bank of England (BoE) this year, while markets also anticipate that the US Federal Reserve may delay or limit monetary policy easing amid inflationary pressures.

Furthermore, a conditional US-Iran ceasefire eased tensions and boosted risk appetite, reducing demand for the safe-haven dollar and supporting the pound.

USD index also came under downside pressure after the release of US Producer Price Index data revealed a softer-than-expected rise of 4.0% during March, reducing the likelihood of higher interest rates which typically support the US dollar. Additionally, US inflation rose to 3.3% in March, its highest in almost two years, as fuel prices pushed up transport and energy costs.

In the UK, the consumer prices index inflation also climbed to 3.3% in March, although softer core inflation led markets to slightly scale back BoE rate hike expectations. Labour data highlighted that unemployment unexpectedly fell to 4.9%, but hiring remained weak, payrolls declined, and wage growth slowed, signalling a cooling labour market.

BoE Governor Andrew Bailey signalled a slowdown in interest rate cuts, stating that it is “too early to form strong judgements” regarding the impact of the wider Middle East conflict on the UK economy, emphasising the need to remain data-dependent amid persistent inflation risks and elevated energy price volatility.

Towards the end of the month, Lloyds revised its 2026 UK inflation forecast to 3.4% from 2.6%, while slashing its GDP growth estimate to 0.5% from 1.2%. Lloyds no longer expects any BoE rate cuts this year, having previously anticipated two.

The BoE and the Federal Reserve both opted to maintain interest rates, the former at 3.75% and the latter at the 3.5%-3.75% range, reflecting caution amid the Iran war. Finally, Andrew Bailey warned that the UK may need to brace for hikes later this year, as “higher inflation is unavoidable.”

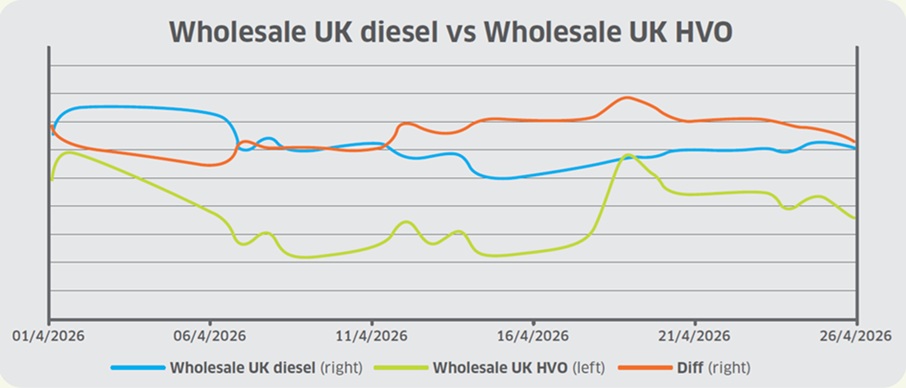

Wholesale UK renewable diesel (HVO) prices (in reference to the HVO UCO Barges FOB ARA benchmark) also fluctuated significantly throughout April, starting at 176.92ppl (excluding duty and Renewable Transport Fuel Certificate (RTFC) benefit), then moving to highs of 182.90ppl and lows of 162.58ppl.

Note: this is a wholesale settlement price comparison only, and does not reflect broader end-user pricing dynamics. The differential between HVO and diesel prices also fluctuated between c.73ppl and c.106ppl throughout the month.

European biofuel prices have risen over the past several weeks, tracking a sharp increase in fossil fuel benchmarks following the escalation of the US-Iran conflict and supply disruptions in the Middle East. At the same time, expectations of tighter compliance-driven demand under strengthening renewable fuel mandates added further support to sentiment in HVO markets.

Global renewable fuel markets are seeing a broader acceleration in blending mandates, with governments tightening long-term policy frameworks to support decarbonisation and energy security. Analysis by Barclays has predicted that global renewable diesel demand will rise by around 35% in 2026, driven primarily by stronger mandates in markets such as the US and Germany.

Expectations that the Netherlands and Germany will abolish the double-counting of waste-based feedstocks this year is also likely to significantly boost HVO demand, as higher absolute amounts of biofuel would be required to meet greenhouse gas reduction quotas.

In late April, the updated Renewable Energy Directive (RED III) was added to Germany’s parliamentary agenda, moving it closer to formal adoption into law. In the Netherlands, legislation amending the Environmental Management Act and the Excise Duty Act has been ratified.

Meanwhile, a biodiesel industry group called on the EU to maintain ambitious renewable fuel targets beyond 2030, warning that existing carbon pricing mechanisms alone are not sufficient to drive the required investment in low-carbon fuels.

The European Biodiesel Board said that continued, dedicated transport fuel mandates under the post-2030 Renewable Energy Directive will be necessary to provide clear demand signals, alongside stronger enforcement, improved certification, and fewer barriers to high-blend biofuel use.

Beyond Europe, policy momentum is also evident in Asia. Indonesia has recently formalised plans to introduce a nationwide B50 biodiesel mandate by 2028, according to a new energy ministry decree, requiring all diesel users to shift to a 50% palm oil-based blend as part of its energy transition strategy.

The phased rollout builds on earlier B40 requirements and reflects efforts to strengthen energy security, reduce fuel imports, and expand domestic biofuel use, with implementation timing structured to allow for feedstock, infrastructure, and industry readiness.

On the supply side, renewable diesel constraints eased following the late-March restart of TotalEnergies’ 500,000 mt/year HVO unit in southern France, after two months’ planned maintenance.

Meanwhile, Italian multinational energy company, Eni, has secured a €500 million, 15-year loan from the European Investment Bank to convert a refinery into a biorefinery, reinforcing Europe’s strategy of expanding HVO supply through the repurposing of existing refining assets rather than new-build capacity.

Despite indications of increased supply into the market, firm underlying gasoil prices amid conflict in the Middle East has kept European prices elevated. European UCO-based HVO prices surged to a four-year high on 22 April, with rising renewable diesel premiums and underlying Low Sulphur Gasoil (LSGO) futures, alongside the impact increased demand from higher blending targets, namely Germany’s recent legislative approval.

Overall, wholesale UK HVO (excluding duty and RTFC benefit) closed at 170.93ppl by the end of April, with the differential versus diesel closing at 87.84ppl, marginally lower than the beginning of the month.

The spot cost of blending biodiesel to the UK B7 specification traded at a negative position at the beginning of April, continuing its trend from March with the rise in wholesale diesel prices (fossil component) significantly outpacing gains in the bio-product (FAME-10).

As the fossil diesel component makes up the majority of the total blend (86.47% for a B7 diesel blend, as of 2026), the widening variance has caused the cost of RTFO to fall dramatically. However, by the end of the month, prices recovered above 1ppl, slightly increasing the spot cost of meeting the Renewable Transport Fuel Obligation.

The price of RTFCs also increased marginally from 16.40 pence per certificate (ppc) to 18.30ppc, slightly increasing the benefit that HVO consumers receive (assuming that 100% of the RTFC benefit is passed on to the end-user).

However, RTFC prices remained low compared to pre-conflict levels. The recent decline in certificate prices can largely be attributed to the significant rise in diesel costs following the Middle East conflict, causing the difference between biodiesel and mineral diesel to narrow, ultimately reducing the cost of blending.