The Middle East conflict continued to weigh heavily on the oil market throughout May, as investors struggled to keep pace with rapidly shifting developments from growing hopes of a ceasefire one day to renewed threats and strikes the next.

At the beginning of the month, oil prices fell after Axios reported that Iran had responded to US amendments to a draft peace plan. However, President Trump said he was dissatisfied with Tehran’s offer, arguing that Iran had failed to make meaningful concessions.

He then announced that ‘Project Freedom’ would begin, a military operation to guide stranded merchant ships through the Strait of Hormuz. However, Trump paused the operation after just two days.

By mid-month, attacks on energy infrastructure across the Persian Gulf, including a nuclear facility in the United Arab Emirates (UAE), supported oil prices. Trump then threatened Iran with “another big hit”, while Iran warned that the US will face “many more surprises” if peace talks fail and US-Israeli attacks resume.

The Strait of Hormuz remains central to the dispute. Reports suggested that Iran had discussed a permanent toll system with Oman for ships using the strait, potentially formalising Tehran’s control over the passage. The proposal alarmed the US and its allies, which argued that passage fees in the strait would be illegal.

International Energy Agency chief Fatih Birol warned that global commercial oil inventories are falling rapidly due to Strait of Hormuz disruptions, with only “weeks” of supply left despite recent emergency reserve releases.

The agency warned that global oil markets are likely to remain in a deficit until Q4, with record stock drawdowns and peak summer demand potentially intensifying supply pressures.

Signs of improvement in global oil supply flows emerged after satellite data showed three Chinese tankers passed through the strait, carrying roughly six million barrels of crude. However, overall traffic remains severely constrained; daily vessel transits remain at around 11 versus 125-140 pre-conflict, with thousands of vessels stranded in the Gulf.

Towards the end of May, further reports by Iran’s state media suggested that the country was committed to restoring commercial shipping via the strait.

Iran reportedly drafted an unofficial framework agreement with the US that would see Washington withdraw military forces and lift its naval blockade in exchange for Tehran restoring commercial shipping through the strait within a month.

On 28 May, reports indicated that the US and Iran had tentatively agreed to extend their ceasefire by 60 days, and that Iran would clear all mines from the vital waterway within 30 days.

However, President Trump had not yet approved the proposed terms, and Vice-President JD Vance warned that it remains unclear whether or when a US-Iran agreement will be finalised.

Overall, oil prices declined by c.17% throughout May, marking the largest monthly drop since 2020 as optimism grew that some form of deal could eventually be reached.

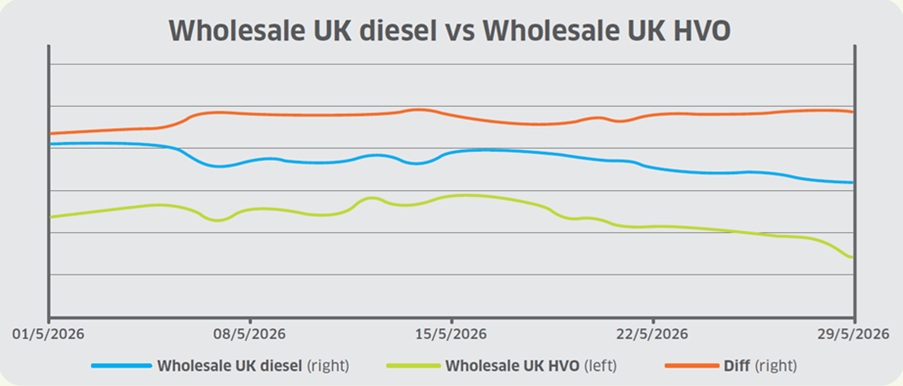

Major hurdles remain, however, including Tehran’s nuclear ambitions, control of the Strait of Hormuz, and sanctions relief. Wholesale UK diesel prices largely tracked Brent crude’s downward trajectory, declining by almost 18ppl to close at 64.39ppl excluding duty.

In other news, the UK government opted to postpone the planned 5ppl increase in fuel duty until the end of 2026. It has also loosened sanctions on diesel and jet fuel refined from Russian crude for an “indefinite” period, a change likely aimed at easing supply pressures and stabilising fuel availability amid ongoing global energy volatility.

Against this backdrop of easing energy prices and geopolitical developments, currency markets remained highly sensitive throughout May. GBP depreciated from US$1.362 to US$1.344 over the month as weaker UK economic data, political uncertainty and shifting interest rate expectations weighed on sterling.

Although periods of softer US dollar sentiment provided some support to the pound, stronger US economic data and a more hawkish Federal Reserve outlook ultimately drove GBP lower over the month.

At the start of May, reports of a potential US-Iran agreement reduced safe-haven demand for USD. However, markets became increasingly cautious over the UK outlook, with investors scaling back expectations for further Bank of England tightening as policymakers expressed scepticism over the UK’s stronger-than-expected growth data.

Investors anticipate just two rate interest hikes by year-end, down from up to three hikes forecasted previously.

Mid-month, sterling came under significant pressure via growing political instability after poor local election results for the Labour party. Speculation surrounding the future of Prime Minister Keir Starmer increased investor concerns regarding future fiscal policy and economic stability.

At the same time, stronger-than-expected US inflation data reinforced expectations that the US Federal Reserve would maintain a tighter monetary policy stance for longer, boosting the dollar and driving GBP lower.

Wholesale UK renewable diesel (HVO) prices (in reference to the HVO UCO Barges FOB ARA benchmark) also declined across the month, from 169.93ppl (excluding duty and Renewable Transport Fuel Certificate (RTFC) benefit) to 162.33ppl by the end of May, despite trading near 174ppl mid-month.

Note: this is a wholesale settlement price comparison only, and does not reflect broader end-user pricing dynamics.

Meanwhile, the differential between HVO and diesel rose from 87.59ppl to 97.95ppl, as diesel prices fell more sharply than HVO.

In its latest Short-Term Energy Outlook, the United States Energy Information Administration raised its forecasts for renewable diesel and biodiesel production for the remainder of the year, while also increasing its renewable diesel import outlook, signalling continued strength in demand.

Renewable diesel production and imports are expected to rise sharply to comply with the US Environmental Protection Agency’s record-high biofuel blending mandate released at the end of March.

That requires refiners to blend record volumes of biofuels into gasoline and diesel this year and next, calling for the “highest volumes of renewable fuels in history” and including a 60% increase in biodiesel and renewable diesel use.

US feedstock pricing has also continued to climb, with sources reporting stronger demand than supply since the US biofuel blend mandate was released, despite an increased presence of imported European and Asian feedstocks.

Although renewable diesel prices declined in the last week of May amid a significant retreat in underlying gasoil futures markets, market participants remain optimistic about the short-term outlook because of strong policy signals, namely Germany’s decision to raise its 2026-2040 renewable fuel targets towards the end of April.

The spot cost of blending biodiesel to the UK B7 specification recovered in May, rising from below 2ppl to almost 5ppl, as wholesale diesel prices (fossil component) fell moderately across May, whereas the bioproduct (FAME-10) rose slightly.

The spot price of the Renewable Transport Fuel Obligation has risen to its highest level since before the outbreak of the conflict in the Middle East, increasing the cost of meeting the Obligation.

The price of RTFCs also increased marginally from 18.30 pence per certificate (ppc) to 18.90ppc, slightly increasing the benefit that HVO consumers receive (assuming that 100% of the RTFC benefit is passed on to the end-user). However, RTFC prices are still trading relatively low versus pre-conflict levels of above 24ppc.