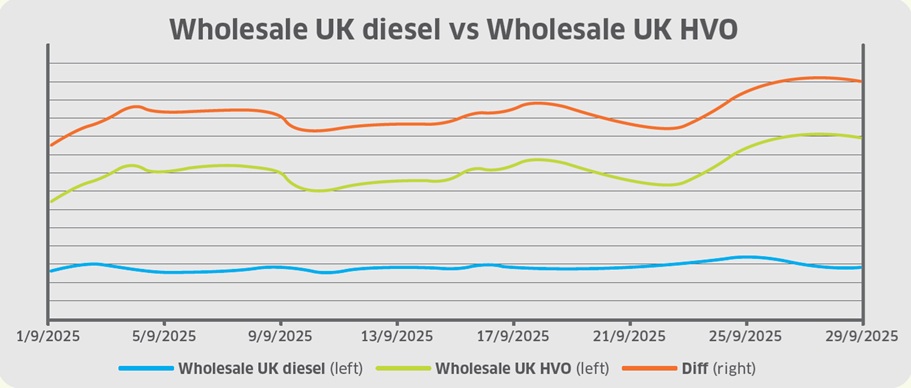

Across September, wholesale UK diesel prices increased from 51.5ppl (excluding duty) to 52.5ppl, a marginal gain that largely tracked the underlying Brent crude benchmark before oil prices fell at month-end and contrasting with a spike in HVO led by rising consumption and pressure on supply.

At the beginning of September, escalating Russia-Ukraine conflict saw several attacks on major energy infrastructure, causing supply disruption. However, oil prices declined following reports that OPEC+ was considering raising its output level again to reclaim lost market share.

The group later announced a 137,000 barrels per day (BPD) hike, less than expected, yet still stoking fears of an oversupplied market heading into the winter, with investors anticipating reduced demand outside of the peak summer period.

Meanwhile, US President Trump called on EU nations to impose tariffs of up to 100% on China and India to force President Putin to end the war in Ukraine. Trump stated that he preferred lower oil prices to additional US sanctions to pressure Russia, causing oil prices to fall.

Towards the end of the month, Iraq increased oil exports after OPEC+ relaxed the quota. However, a deal to resume exports from Iraqi Kurdistan stalled due to debt repayment assurances, preventing 230,000BPD from re-entering the market via Turkey.

Although Kurdish supplies eventually resumed after oil operators struck an export deal with Baghdad, improved US demand with declining crude stocks and persistent geopolitical concerns helped oil prices recover marginally.

GBP weakened from US$1.355 to US$1.346 throughout September, losing ground after a strong performance in August and contributing marginally to higher UK diesel prices.

At the beginning of the month, broad US dollar weakness supported the pound due to expectations that the US Federal Reserve would cut interest rates amid persistently weak labour data.

For example, the US economy added just 22,000 jobs in August compared to forecasts of 75,000, and unemployment rose to the highest level since 2021 at 4.3%. Inflationary data also increased the likelihood of interest rate cuts as the US Consumer Price Index rose by just 0.2% to 2.93% and core inflation remained at 3.1%.

As a result, Federal Reserve officials opted to cut interest rates by 25 basis points, as widely expected.

Meanwhile, the central bank’s independence continued to be threatened by Trump. The President pursued control over the Fed, with ongoing criticism of Chair Jerome Powell. Additionally, the Justice Department opened a criminal fraud investigation into Governor Lisa Cook, who Trump sought to fire over mortgage fraud allegations.

In the UK, August inflation was recorded at 3.8% year-on-year, remaining at a 19-month high and almost double the Bank of England (BoE) 2% target. Despite Office for National Statistics data showing a weakening labour market, BoE opted to hold interest rates at 4%.

Although diverging monetary policy between the UK and US supported the pound, fiscal uncertainty caused GBP to weaken, and pressure continued to mount for Chancellor Rachel Reeves ahead of the Autumn Budget in November.

Wholesale UK renewable diesel (HVO) prices increased from 132ppl (excluding duty and Renewable Transport Fuel Certificate (RTFC) benefit) to almost 149ppl by the end of the month, largely due to strong European demand guided by the EU Renewable Energy Directive (RED).

Obligated parties are rushing to meet member states’ respective biofuel blending mandates before year-end and before prices rise further. Additionally, authorities in the Netherlands have started exploring the possibility of extending the nation’s renewable transport fuel targets under RED out to 2040 to better align with countries such as France and Germany.

Furthermore, increased HVO consumption has contributed to tighter supplies in Europe, and planned maintenance closures at several European and Chinese facilities during Q4 may continue to support prices into 2026.

Supply continues to be impacted following the UK Trade Remedies Authority (TRA) investigation into biodiesel shipments from China proposing the introduction of anti-dumping duties on Chinese imports of fatty acid methyl esters and HVO.

Prior to a final recommendation being made, TRA requested comments or additional evidence from stakeholders in September.

In the United States, after a bearish Q1, renewable diesel production has been ramping up and slowly returning to 2024 levels. However, US demand has stagnated due to policy uncertainty around 45Z incentives, blending mandates, and increased exports.

The Energy Information Administration (EIA) reports that consumption is expected to improve in the months ahead, to meet existing mandates under the US Renewable Fuel Standard programme.

Finally, the cost of blending biodiesel to the UK B7 specification rose marginally from 7.6ppl to 7.8ppl, increasing the cost of meeting the Renewable Transport Fuel Obligation (RTFO). Meanwhile, the price of RTFCs lifted from 25ppc to 26ppc, slightly increasing the benefit that HVO consumers receive (assuming 100% of the RTFC benefit is passed to the end user).