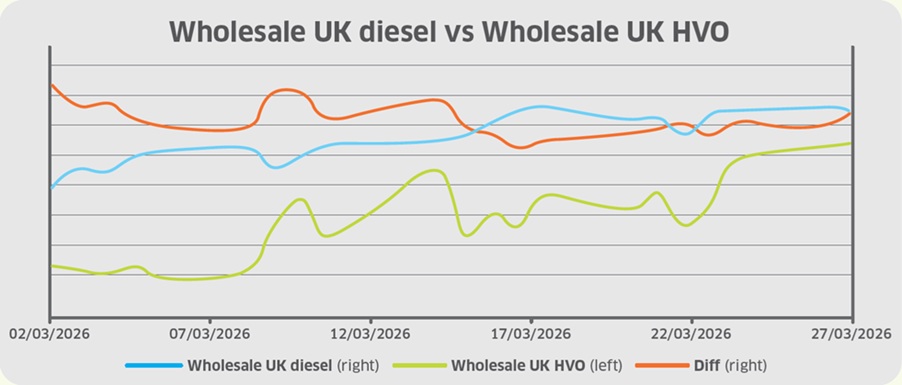

In March, wholesale UK diesel prices rose significantly from 56.23ppl (excluding duty) to 89.10ppl. That largely tracked the underlying Brent crude benchmark, which increased by around 50%, marking the largest gain since May 2020 when prices rebounded sharply following the crash driven by COVID-19.

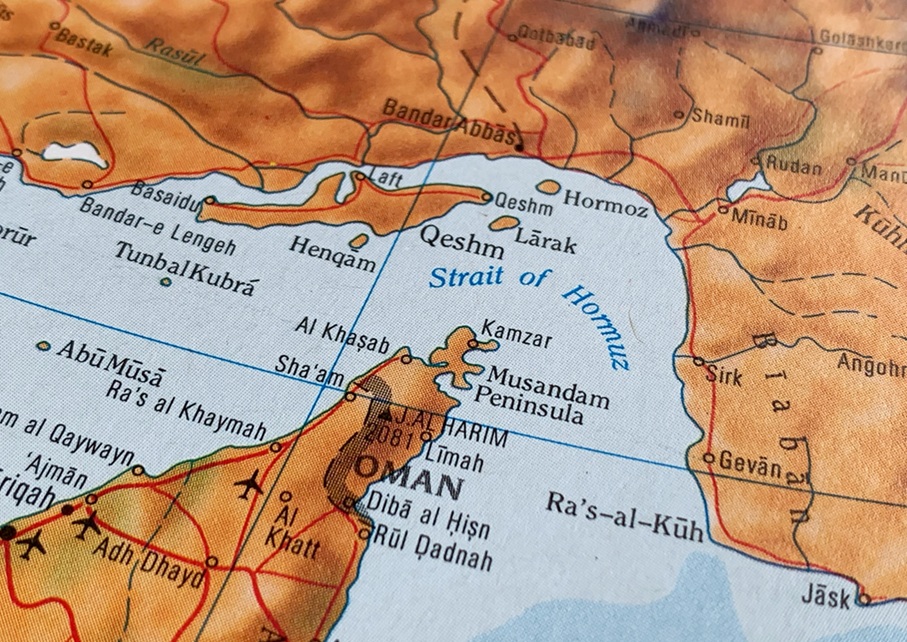

Energy markets remained extremely volatile as a result of war in Iran and the effective closure of the Strait of Hormuz. Tehran originally insisted that it remained open, but multiple vessels were targeted. Iran’s Revolutionary Guards Corps later claimed “complete control” of the strait, warning that any vessel passing through would be targeted.

Meanwhile, President Trump pledged that the United States would safeguard shipping via the strait, helping oil prices to ease slightly. However, he also stated that the US would not pursue any diplomatic agreement with Iran unless the country agreed to an unconditional surrender, heightening tensions once again.

On 10 March, oil prices briefly dipped by 10% to below US$89 per barrel after Trump claimed the war with Iran would “end very soon.” However, production cuts from major Middle Eastern producers pushed prices above US$100 on 12 March for the first time since July 2022.

Despite 32 nations coordinating with the International Energy Agency to release 400 million barrels of strategic oil reserves, that measure had little impact on prices.

Lack of clarity on Middle East conflict resolution hurts prices

Later in March, Israel expanded operations against Iran-backed Hezbollah in Lebanon, while Iranian strikes targeted energy facilities in the United Arab Emirates, signalling that the conflict was broadening across the region. Iran’s army chief also vowed “decisive” retaliation for the killing of security chief Ali Larijani, as Tehran intensified threats.

Trump then signalled de-escalation by ordering a five-day pause on planned US strikes against Iranian energy infrastructure, suggesting “productive” talks had been held with Tehran for the “complete and total resolution” of hostilities. While oil prices initially eased, Iranian officials denied claims of any talks to end the conflict.

The US later opted to extend the pause on strikes until 6 April, while urging Iran to engage “seriously” in talks “before it is too late”. Reports then emerged of a 15-point plan delivered to Iran via Pakistan, including missile limits, nuclear rollback, and sanctions relief.

Looking ahead, Israeli Prime Minister Benjamin Netanyahu stated that the war is “definitely beyond the halfway point”, but later confirmed that was in terms of missions, not timeframe. Meanwhile, Israel’s military spokesperson says the country is “prepared to keep operating for weeks to come”.

Finally, reports emerged that Trump told aides he is willing to end the US military campaign against Iran even if the Strait of Hormuz remains largely closed, potentially strengthening Tehran’s control over the vital waterway.

However, Trump continues to oscillate between threats of escalation and suggestions of a near end to hostilities, causing significant uncertainty.

The Middle East conflict has increased global financial volatility and strengthened safe-haven demand for the US dollar, putting pressure on other major currencies. Across March, GBP fell from around US$1.337 to US$1.320 amid heightened risk aversion and market uncertainty.

UK ‘particularly exposed’ to impact of Middle East conflict

The UK’s Office for Budget Responsibility cut its 2026 growth outlook and warned that higher energy prices could significantly weigh on activity, a view broadly echoed by the Organisation for Economic Co-operation and Development. It sees the UK as particularly exposed among major economies, forecasting economic growth this year at just 0.7%.

At the same time, inflation remains stubborn, with the consumer price index (CPI) at 3.2% and food inflation accelerating to 4.3% in the 12 months to February, limiting the scope for the Bank of England (BoE) to pivot towards monetary policy easing.

On 18 March, the BoE’s Monetary Policy Committee voted unanimously to maintain interest rates at 3.75%, with Governor Andrew Bailey signalling that future moves depend on how long energy-driven inflation persists.

Meanwhile, Prime Minister Keir Starmer warned that the UK economy could dampen if the Middle East conflict persists, but the government suggested that short-term energy costs are partly cushioned by the UK energy price cap.

Towards the end of March, Starmer chaired an emergency Cobra committee meeting, attended by BoE Governor Andrew Bailey and senior ministers, to discuss the impact of the Iran war on the domestic economy.

HVO price volatility seen in March via multiple factors

Wholesale UK renewable diesel (HVO) prices (in reference to the HVO UCO Barges FOB ARA benchmark) also experienced significant volatility in March, rising from 158.21ppl to 177.85ppl (excluding duty and Renewable Transport Fuel Certificate (RTFC) benefit).

However, the increase in fossil diesel prices outpaced HVO, and therefore the differential between the pair narrowed. Note: this is a wholesale settlement price comparison only, and does not reflect broader end-user pricing dynamics.

At the beginning of March, renewable diesel prices recorded relatively small moves as their premiums fell to offset stronger fossil diesel prices. While the rise in oil prices is generally supportive for renewable diesel prices, a hit to diesel supply and sales in Europe could also slow down the need for biofuel blending in middle distillates in the short term.

From mid-month, European renewable diesel prices surged to reach multi-year highs, with used cooking oil-based HVO at its highest level since 2022.

The European biofuel industry was already anticipating a tight market this year, as new, higher renewable fuel targets due to the third EU Renewable Energy Directive are implemented across the bloc. For example, Germany has prepared for higher road-fuel GHG reduction and biofuel targets to accelerate renewable fuel deployment.

In the US, as part of the Environmental Protection Agency (EPA) Renewable Fuel Standard (RFS) “Set 2” regulations, record-high biofuel mandates were announced towards the end of March, raising Renewable Volume Obligations for 2026 and 2027 to support domestic agriculture and renewable fuel production.

As targets have increased, domestic demand for HVO and biodiesel in the US has surged, causing feedstock prices to rise.

An amendment to the EPA’s renewable fuels policy also effectively removed the previous restriction on imported feedstocks, enabling the same level of credit generation from both domestic and imported feedstocks for Renewable Identification Numbers (RIN), used by obligated parties to prove compliance with EPA mandates.

Due to insufficient domestic supply to meet the additional demand, US producers are increasingly relying on imports to meet the new targets, which will likely impact the availability of feedstock supply to Europe and increase HVO production costs.

In the UK, the Trade Remedies Authority (TRA) initially recommended that duties between 20-32ppl to be applied on US HVO, therefore T1 (non-EU) cargoes were being offered with a duties protection uplift to offset the TRA, narrowing the price gap versus T2 (EU) product, albeit still at a discount.

However, in mid-March, TRA advised against imposing countervailing duties on US HVO exports to the UK, and the gap widened. Despite the its decision, the EPA’s announcement of the new RFS regulations saw the differential narrow once again by the end of the month, following an expected increase in demand from the revised RFS.

Biodiesel blending costs plummet alongside RTFO impact

The cost of blending biodiesel to the UK B7 specification plummeted throughout March, trading below 1ppl, and even falling into a negative position on 30 March, drastically reducing the spot cost of meeting the Renewable Transport Fuel Obligation (RTFO).

Since the start of the Iran conflict on 28 February, the rise in wholesale diesel prices (fossil component) has significantly outpaced gains in the bio-product, which has broadly remained flat. As the fossil diesel component makes up the majority of the total blend (86.47% for a B7 diesel blend, as of 2026), the widening variance has caused the cost of RTFO to fall dramatically.

The price of RTFCs has also declined, from 24.40ppc to 16.20ppc, significantly reducing the benefit that HVO consumers receive (assuming that 100% of the RTFC benefit is passed on to the end-user).

Weak market sentiment for domestic renewable fuel producers and lower compliance costs reduced demand for RTFCs. Meanwhile, TRA’s decision to recommend against imposing anti-subsidy duties on US HVO contributed to lower prices. As cheaper US imports remain available, supply constraints are eased and certificate scarcity is ultimately reduced.