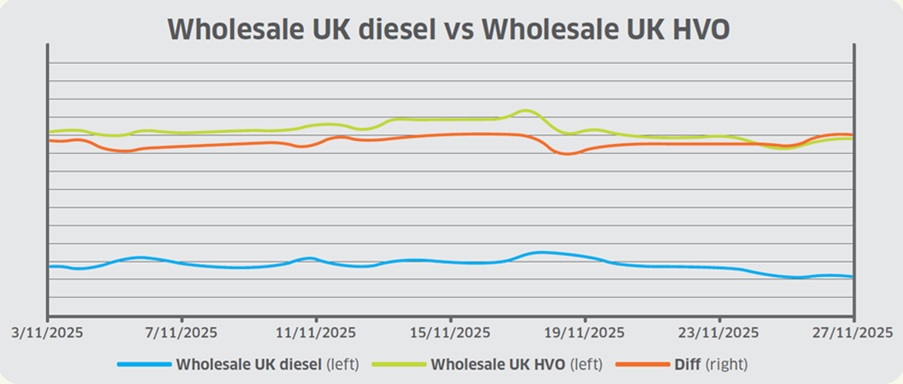

Wholesale UK diesel prices fell from 55.47ppl (excluding duty) to 52.33ppl during November, despite climbing towards 60ppl on 18 November. The underlying Brent crude benchmark followed a similar downward trajectory as markets faced shifting supply signals, geopolitical developments, and mixed demand factors.

Early in the month, OPEC+ confirmed a 137,000 barrel per day (BPD) output hike while signalling a pause in further output increases for Q1 2026. However, caution remained over excess supply combined with weakening global demand, prompting prices to retreat.

In the United States, news that the longest government shutdown in history was coming to an end boosted demand optimism in the world’s largest crude-consuming nation.

Meanwhile, US sanctions on Russia continued to target seaborne exports and oil majors Rosneft and Lukoil, providing support to oil prices. As a result of Western sanctions, Moscow’s oil revenues fell to their lowest level since August.

However, Brent prices plummeted after OPEC+ forecast a 500,000BPD supply surplus in global oil markets in Q3, in stark contrast to last month’s estimate for a 400,000BPD deficit.

Although geopolitical tensions prevented oil prices from free-falling, namely Ukrainian strikes on critical Russian energy infrastructure, oversupply concerns weighed on the market. Additionally, reports that loadings had resumed at Russia’s Novorossiysk port exacerbated supply glut concerns.

In the final week of November, Brent traded around a one-month low due to increased optimism over a Russia-Ukraine peace deal, which could see the lifting of Western sanctions on Russia and add more supply to the market.

On the last day of the month, OPEC opted to maintain existing output levels, slightly reducing concerns.

GBP strengthened from US$1.314 to US$1.325 throughout November. Volatility was evident as the pound fluctuated between seven-month lows and a one-month high. At the beginning of the month, investors were cautious after Chancellor Rachel Reeves hinted at potential tax hikes ahead of the autumn Budget and refused to rule out a U-turn on Labour’s manifesto pledge not to increase income tax, VAT or National Insurance.

Meanwhile, the Bank of England narrowly voted to keep interest rates at 4%, as some policymakers see CPI inflation peaking, though further easing could be needed if disinflation continues.

Weak UK labour data, including slower pay growth and unemployment reaching 5%, increased the likelihood of a December rate cut. Soft GDP figures, with Q3 growth at 0.1% and September output contracting, weighed on sentiment.

UK inflation fell to 3.6% in October, its first drop since March, driven by smaller household energy cost increases after Ofgem’s price cap adjustment. In the US, Goldman Sachs forecast Federal Reserve rate cuts in December alongside two additional cuts in March and June 2026, weakening the dollar.

Towards the end of the month, investors digested Rachel Reeves’ Budget. It targeted Britain’s wealthiest households with £26 billion of tax raising to fund scrapping the two-child benefit policy and cutting energy bills, while extending the 5ppl fuel duty cut (introduced in 2022) until September 2026.

The Office for Budget Responsibility warned the Budget leaves public finances vulnerable, forecasting slower UK growth due to lower productivity.

Wholesale UK renewable diesel (HVO) prices also declined across the month, from almost 151ppl (excluding. duty and Renewable Transport Fuel Certificate (RTFC) benefit) to just above 149ppl as market participants noted softening demand moving towards the end of the year.

In Europe, renewable diesel prices climbed last month due to tight supply, strong waste feedstock prices and higher targets set to be introduced next year under the new RED III policy.

However, a German cabinet meeting to discuss the RED III transposition was again delayed in mid-November, having initially been scheduled to be held in early October. Additionally, despite market speculation, the German government has no specific plans to confirm new renewable targets at a meeting in early December.

In other news, the UK Trade Remedies Authority (TRA) plans to recommend that the government places a countervailing duty on US-origin HVO, with TRA set to prepare the final recommendation in March 2026.

Separately, TRA has terminated its parallel investigation into dumped imports of HVO biodiesel from the US due to a lack of significant evidence of dumping.

Finally, the cost of blending biodiesel to UK B7 specification rose marginally from 7.6ppl to 7.9ppl, slightly increasing the cost of meeting the Renewable Transport Fuel Obligation.

Meanwhile, the price of RTFCs decreased from 27 pence per certificate (ppc) to 26ppc, decreasing the benefit that HVO consumers receive (assuming 100% of the RTFC benefit is passed on to the end-user).